Throughout the years, payment methods have constantly evolved to keep up with the demands of an ever-changing society. Cash, being the most traditional form of payment, has been declining, while credit cards and mobile payments have been increasing and are expected to continue in the coming years. This shift in payment methods has changed how people make purchases and opened up many opportunities for businesses to offer their customers more convenient and secure payment methods. There are, of course, many other benefits that are included when accepting credit cards at a business. However, store owners may be hesitant to accept credit cards due to the processing fees, long-term contracts, and hidden fees that can impact their bottom line. In this article, we will explain why it will be beneficial for a business owner to accept credit cards, what is involved in the process, and what we can offer.

Why Should a Small Business Accept Credit Cards?

No matter what type of business a merchant has, it’s important to accept customer credit card payments. Around the world, credit cards have become the most preferred payment method because of their rewards, security, and convenience. Oftentimes, customers are encouraged to use their cards, especially because of the offers and rewards that come with them. The rewards programs available to customers allow them to receive points for every purchase made, which can then be redeemed for cash back or discounts on their next purchases. Additionally, customers are guaranteed safety and security when making purchases with their cards. Paying with a card comes with many layers of security that will guarantee that their financial and personal information is protected against fraud and theft. When a business accepts credit cards, customers can make purchases quickly and efficiently by swiping, tapping, or dipping their cards. They will also be more satisfied that they have more payment options than carrying cash. So it is no wonder customers enjoy using their cards while checking out.

If merchants are still not convinced about accepting them, they should read along to understand all the reasons how it can help their business:

1. Credit Cards Are More Secure

When customers use their cards, it comes with numerous benefits that allow them to track their spending, receive more funds, dispute fraudulent transactions, and protect their personal information from hackers. If, for some reason, a customer loses their card, they can always dispute it with their credit card company and ensure that no one else can have access to their funds. The same goes for merchants who want to apply for a business credit card. They can also benefit from the same protections, which allow them to easily manage their finances and accounts. If it is a cash-only business and there is a robbery, merchants may find it difficult to recoup their losses and, unfortunately, will have no protection. This money will be forever lost, and business owners will feel helpless and vulnerable. That is why credit cards are the preferred payment method because of the many layers of security they provide. This includes data encryption such as personal identification number (PIN), chip, and signature that helps customers protect their data.

2. Credit Cards Are More Convenient

In today’s digital age, a cash-only business cannot compete with its counterparts, who accept digital payment options such as credit cards, online transfers, and mobile payment services. Especially since since 80% of customers prefer using a credit card over cash. Customers would rather go to a store with more payment methods than one that limits their options.

Customers can also pay for items using an app on their phone that carries their card information digitally, such as Apple Pay, Google Pay, Amazon Pay, etc. Customers that pay with their cards not only can speed up the checkout process but also help the business expand its consumer base, resulting in more revenue.

3. Credit Cards Let You Track Your Spending

When customers pay with cash, there is no record of how much money they have spent. Rather, customers have to manually input how much they spent through an app or keep paper receipts, which is time-consuming and, in many cases, unreliable. On the other hand, customers who use their cards can track their spending by looking at their payment history, using their credit card’s mobile app, looking at receipts, and so on. Credit card companies that have an app for their customers can send notifications to their phones if a purchase has been made. This allows customers to track their spending better and prevents them from overspending unknowingly. Customers prefer to pay with their card when purchasing from a store since it gets recorded in their credit transaction history.

4. Credit Cards Build Your Credit History

Using a credit card has many benefits, but one of the most important is building a credit history. Merchants and customers can both benefit from using their cards because it can provide them with loans for whatever they need to help grow their businesses or purchase necessary items. Building a credit history can offer them more access to potential funds in the future as their creditworthiness increases.

5. Credit Cards Come With Rewards

Finally, credit cards give customers rewards that encourage them to use their cards when making purchases. Many credit card companies provide various rewards, such as cashback, airline points, sign-up bonuses, discounts, etc. There are many credit card companies to choose from, each of which can benefit any consumer based on their specific needs. For example, if a customer spends most of their money at grocery stores and gas stations, a credit card company caters to these purchases and provides cash back. Business cards are also available for store owners and entrepreneurs that offer rewards specifically tailored to their business needs.

What Equipment Do I Need to Accept Credit Cards?

There are numerous methods that a business can use to accept credit cards in their store. Accepting credit cards begins with choosing a processor and point-of-sale system, followed by determining which pieces of equipment a store owner may need to improve the checkout process. For example, they may need a card reader, POS terminal, cash drawer, and printer for receipts.

Credit Card Reader

A credit card reader is a machine that decodes a customer’s card information from the microchip, magnetic stripe, etc. When a customer inserts or swipes their card, the credit card reader reads the data from the chip or magnetic stripe and sends it to the payment processor. It then collects the customers’ bank information, and the transaction will be approved if there is enough money on the card. The credit card processor will then notify the customer and return the information to the employee to finish the sale. While these machines are secure, it’s always important for store owners to ensure that they have a credit card reader that is capable of reading EMV chip cards. If the card reader has this function, it can prevent fraud by generating a new code for each customer transaction. This can make them less vulnerable to having their information stolen by hackers. There are ways to manually enter credit card numbers on a computer, like consumers have become accustomed to doing on Ecommerce sites. However, manually entering information is an inconvenient and inefficient way to process credit cards. The best way to process credit cards is with a suite of equipment that works in concert to make the checkout process as quick and convenient as possible. Before we discuss the other pieces of equipment that can assist in the process, let’s focus on the essential piece of equipment you’ll need: a credit card reader.

Credit Card Reader

A card reader is called such because it reads the information embedded in a credit or debit card, either through a microchip, magnetic strip or both. This device is what customers interact with. They insert or swipe their card when prompted and confirm the amount of the payment. This card reader initiates the process of authentication, which we’ll discuss more in the next section.

Merchants should make sure they have a card reader that is capable of reading EMV chip cards, since these cards are becoming increasingly popular over the traditional magnetic stripe cards you swipe. According to credit card giant Visa, three-quarters of U.S. storefronts now have the necessary equipment to process EMV cards. The trouble with magnetic stripe cards is that the information they contain never changes, so getting the details once is enough for someone to copy it and use it for fraudulent charges. EMV cards prevent fraud by generating a new code each time a person uses it to buy something. That way, information from one transaction won’t be useful to someone wanting to commit fraud by using it repeatedly.

Other Components Used to Facilitate Credit Card Sales

If merchants want to further enhance their customers’ checkout experience, there are other components they should consider using. These components include a barcode scanner, POS terminal, customer-facing screen, cash drawer, and receipt printer. Having these at a store can allow merchants to quickly and accurately scan items, process payments, and print receipts to make customer transactions as seamless as possible. Below, we will discuss why these are necessary for any marketplace to keep operations running smoothly and efficiently:

Barcode scanner: Merchants can easily scan products with a barcode scanner instead of manually entering product information. They can even generate their own barcodes and scan the product, which integrates with the NRS POS system for a seamless checkout experience. Merchants can also track their products using an inventory management system, which logs each item. This not only simplifies the checkout process but also helps merchants save time and money by reducing the amount of manual labor needed.

POS terminal: The all-in-one POS system includes hardware and software to assist merchants in managing their business operations more efficiently. The terminal is a touchscreen that is customizable and comes with numerous tabs. This can include registrar, store statistics, vendors, inventory management, in-store items, price-book, and managing discounts.

Customer-facing screen: The NRS POS has two screens, one for employees and one for customers. The customer-facing screen includes transaction information, discounts, and advertisements. This makes the checkout process more interactive for customers while they wait in line and provides the transparency that customers value.

Cash drawer: Cash drawers must be reliable and sturdy enough to hold up to regular use and secure enough to keep the money safe from theft or tampering. They are required for any merchant who wishes to operate an efficient checkout process. The NRS cash drawer is made of stainless steel, temperature-resistant, easy to clean, and long-lasting.

Receipt printer: These printers provide customers with accurate receipts while checking out and use special ink that speeds up the checkout process. Instead of traditional ink, the NRS thermal receipt printer employs thermal technology, which uses heat to print images and text, eliminating the need for a ribbon or toner.

How Does Low Rate Credit Card Processing Work?

Now, store owners should have an idea as to why credit card processing is important to have and how the equipment can help them improve their services. It is also vital for store owners to know how the process works and how they can avoid paying high transaction fees that can ultimately hurt their bottom line. Let’s go through the stages one by one for store owners to get a clear understanding of what the process is like:

1. Authorization

The customer first inserts or swipes their card into the credit card processor. The processor collects the data from the card and transmits it to the credit card network. The credit card network then submits a request to the credit card issuer. The issuer reviews the card information: card number, expiration date, billing address, CVV, and payment amount.

2. Authentication

The issuer then requests the payment from the customer’s bank. The bank looks over the information and approves the account and the funds available to make the payment. The bank will hold the funds in the customer’s account until the store owner’s point-of-sale system approves it.

3. Clearing and Settlement

The store owner’s point-of-sale system sends the approved authorization to the payment processor. The payment processor sends the information to the credit card company and then to the bank. The funds are transferred to the store owner’s account, which typically happens within 24 to 48 hours.

Fees Explained

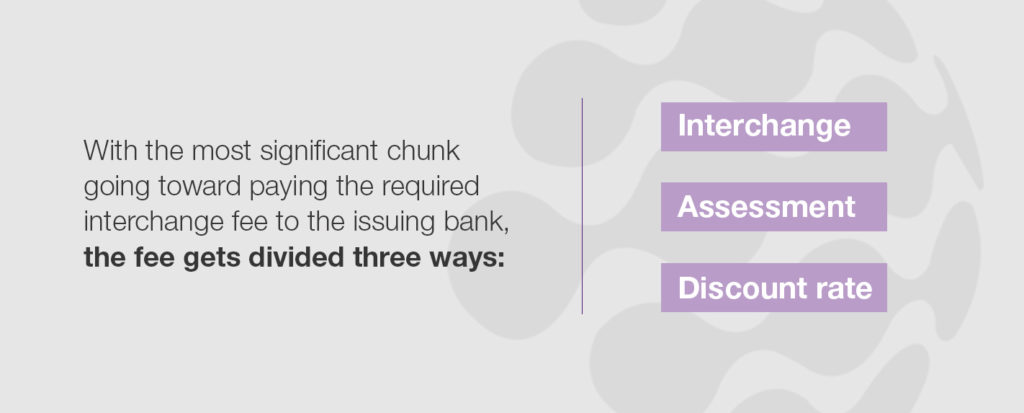

The transaction fees are deducted from store owners whenever a customer pays for an item. These fees usually go to the banks and processors involved in the transaction and are divided into three categories. The most significant amount goes towards paying the interchange fees to the bank.

Interchange: These are transaction fees that the merchant’s bank must pay when customers use their debit or credit card. The fee is usually 2% but depends on the credit card company and is non-negotiable. These fees are calculated by a few factors: credit or debit cards, rewards cards, merchant category code (MCC), etc.

Assessment: Credit card companies also set these fees, which are non-negotiable. The fees go to the credit card company and are smaller than interchange fees.

Discount rate: The discount rate is a fee credit card companies charge along with the interchange and assessment fees. This fee can also be referred to as a markup with a flexible negotiation rate.

Processors will use one of these models to determine their fees.

Interchange plus: Interchange plus models vary monthly and are complicated to understand and read on a statement. However, it can be the most cost-effective option for retailers who move many products every month or sell high-dollar items.

Flat rate: Flat rate models keep things simple and are an excellent choice for merchants with low-ticket items. For every transaction, retailers pay one predetermined fee.

What Options Are Available From NRS?

When customers choose the wrong credit card processing company, they can be hit with hidden fees and markup fees that can hurt their bottom line. At NRS, we strive to be transparent and honest with our customers. We offer no hidden or markup fees or additional charges. That isn’t all; we also offer transparent terms and conditions and a customer support team that can help our customers understand all the features of our credit card processing service. We also have two pricing options for credit card processing so that merchants can choose the best fit for their business:

Flat rate: The flat rate is one fee that never changes, so merchants know what fee they’ll pay every time, whether someone swipes, taps, or dips their card. This flat rate is 2.49% of the transaction cost plus $0.10, making it one of the cheapest credit card processing options for small businesses.

Custom rate: If a business processes high volume monthly in credit card transactions, NRS can set a custom rate to fit their business and save them money. Merchants can also get a free quote to determine what this rate would look like for their business.

Cash discount program:

At NRS, we understand how important it is for small businesses to have an affordable credit card processor. So many credit card processing companies take advantage of small businesses, but not us. We want to give our customers everything they need to succeed and compete on a level playing field. Our credit card processors accept all payment methods, including EBT, eWIC, Apple Pay, Google Pay, and others. We also offer small businesses:

Security

POS compatibility

Customer service

We want our customers to have the best experience possible. That is why we strive to provide the highest level of security, compatibility with our point-of-sale systems, and excellent customer service for all of your needs!

Contact NRS Today for Reliable Small Business Credit Card Processing

Credit card processing doesn’t have to be a hassle; with the all-in-one POS system from NRS, we offer merchants the best built-in software and hardware that gives merchants everything they need to effectively manage their business. We offer a thermal printer, barcode scanner, cash drawer, customer-facing screen, and credit card processing from NRS PAY. We have so many features for our customers to choose from, making it easy for merchants to find exactly what they need to suit their business. Our POS system software automatically updates merchants to the latest version to provide customers with excellent service every time. To get started, request a free quote today.